The Wrapper Trade: What You Actually Own When You Buy SpaceX

The biggest public offering in history is here, and the story tells itself. After two decades as the most valuable private company on earth, Space Exploration Technologies Corp. has gone public. It filed its S-1 on May 20, listed on Nasdaq under the ticker SPCX, and became effective in June. A generational company is finally available to ordinary investors. Everyone, the narrative goes, wins.

We are not here to argue that SpaceX is a bad company. It is an extraordinary one. We are here to ask two different questions, the same two we ask of every asset sold into a wave of enthusiasm: what are you actually buying, and who is on the other side of the trade when the enthusiasm fades.

The answers are more interesting than the headline.

What You Are Actually Buying

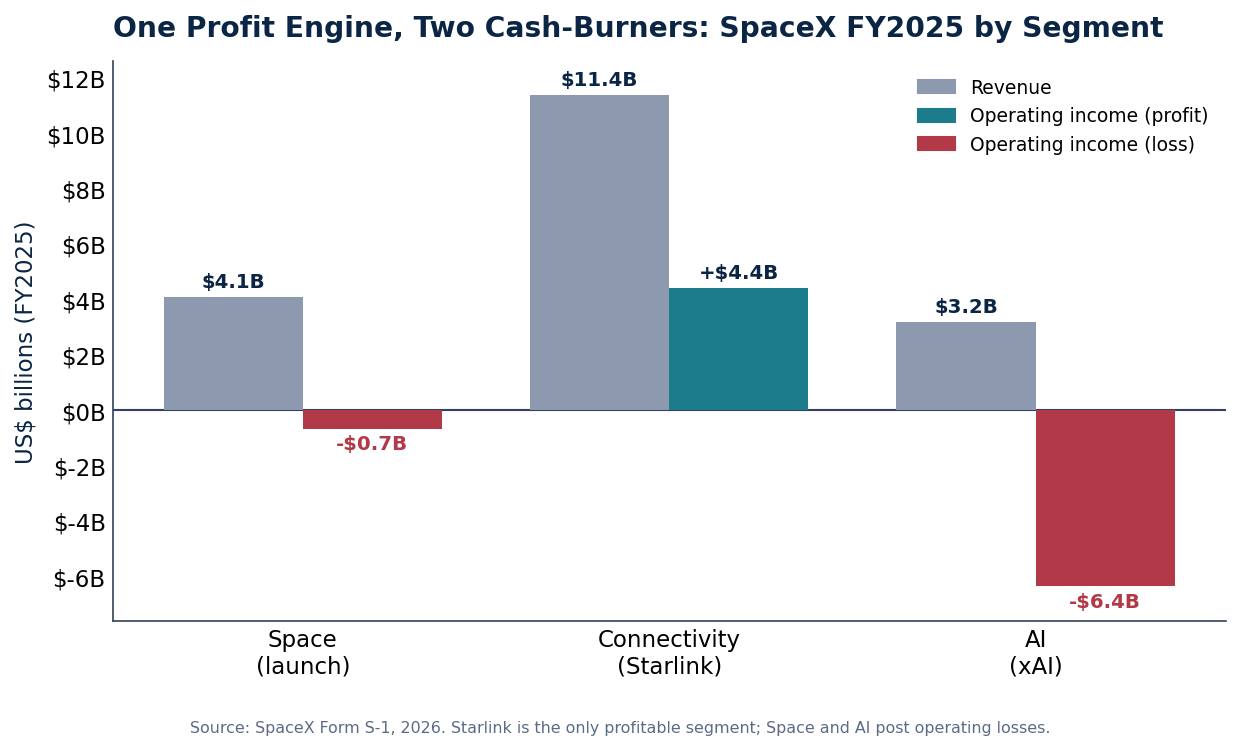

The word "SpaceX" suggests a single thing: rockets. The filing tells a different story. The company reports in three segments, and they are three genuinely different businesses bundled under one ticker. There is Space, the launch business everyone pictures: Falcon, Starship, the reusable rockets. There is Connectivity, which is Starlink, the satellite-internet network. And there is AI, which is xAI and its Grok models, folded into the company through an acquisition completed in February 2026. Buying SPCX is not buying a rocket company. It is buying a conglomerate.

That matters because the economics of the three are not remotely alike. In fiscal 2025, Starlink generated roughly $11.4 billion in revenue and about $4.4 billion in operating income. It is the profit engine, and a real one. The launch business generated roughly $4.1 billion in revenue and lost about $657 million at the operating line. The AI business generated roughly $3.2 billion in revenue and lost about $6.4 billion.

Read that again. One segment makes billions. The other two, combined, lose more than the first one earns. When you buy "SpaceX," you are buying a single profitable business that is being asked to carry two capital-intensive, loss-making ones on its back. The wrapper does not hide a weak company. It hides where the value actually lives, which is a different and more useful thing to know.

| Segment | Business | FY2025 revenue | FY2025 operating income | Role |

|---|---|---|---|---|

| Space | Launch (Falcon, Starship) | $4.1B | -$0.7B | Capital-intensive; small loss |

| Connectivity | Starlink (satellite internet) | $11.4B | +$4.4B | The profit engine |

| AI | xAI / Grok (acquired Feb 2026) | $3.2B | -$6.4B | Deep loss; cash-burning |

This is the same structural point we made about the bank stablecoin launches: the interesting question is rarely the one on the label. There, the label said "Wall Street embraces crypto" and the structure said "incumbents reclaim the rails." Here, the label says "own SpaceX" and the structure says "own Starlink, and subsidize the rest."

There is a second layer the wrapper obscures, and it is governance. SPCX comes with a dual-class share structure. The Class A shares sold to the public carry one vote each. The Class B shares carry ten. The Class B holders elect a majority of the board, and the company qualifies as a "controlled company" under Nasdaq rules, which exempts it from several independence requirements. Elon Musk holds roughly 42 percent of the equity but somewhere in the range of 79 to 85 percent of the voting power.

So the public shareholder buys exposure to the cash flows and essentially none of the control. That is not unusual for a founder-led technology listing, and it is not a scandal. But it compounds the wrapper problem: not only are the segment economics blended, the public holder has no mechanism to influence how capital moves between the profitable segment and the unprofitable ones. You are a passenger, and the seat does not recline.

| Attribute | Class A (public) | Class B (insider / founder) |

|---|---|---|

| Votes per share | 1 | 10 |

| Elects board majority | No | Yes |

The Runup Everyone Expects, and Why It's the Wrong Worry

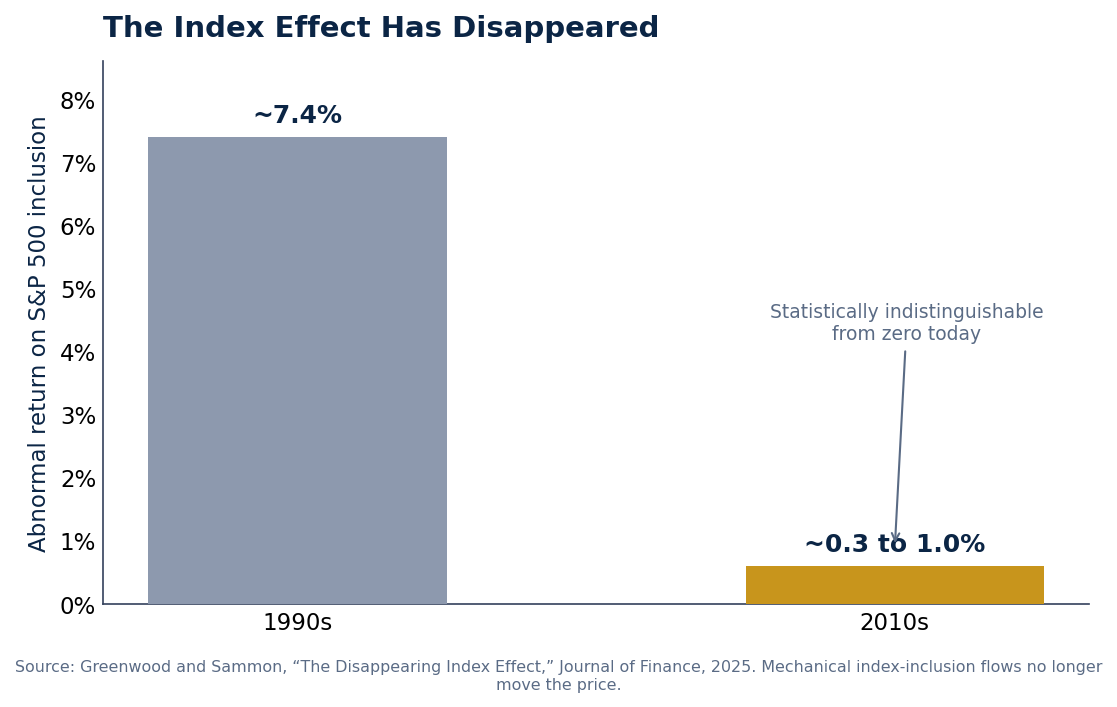

Here is where the conventional bear case, and the conventional bull case, both tend to go wrong in the same way. The common assumption is that the listing will be mechanically lifted by passive flows: index inclusion in the S&P 500 or Nasdaq-100 forces index funds and target-date retirement portfolios to buy, regardless of price, and that wall of price-insensitive money inflates the stock independent of fundamentals.

It is an intuitive story. It is also, on the evidence, mostly obsolete.

The "index effect," the abnormal return a stock earns simply from being added to a major index, has decayed almost to nothing. Work by Greenwood and Sammon documents the arc: an addition was worth on the order of 7 percent in the 1990s, and that premium has fallen to roughly zero in the last decade as indexing scaled and arbitrageurs learned to front-run the rebalances. The mechanical bid is still there. It just no longer moves the price the way folklore insists it does. You do not need a special rule to route retirement money into a newly listed mega-cap, and contrary to some speculation, there is no evidence of one. Index inclusion already does it, quietly, and it barely registers in the price.

So if you are worried about mechanical flows pumping SPCX, you are watching the wrong gauge. The mechanical channel is real but weak. The dangerous channel is somewhere else entirely.

What can carry a stock far above the fundamentals of its profitable core is not a passive index bid. It is narrative demand: buyers who are price-insensitive not because an index forces them, but because they want to own the story. The Musk premium is real. The retail enthusiasm is real. The "I have waited fifteen years to own a piece of SpaceX" impulse is real. None of that is anchored to Starlink's operating income, and that is exactly the point.

Tesla is the cautionary precedent, and it cuts against the lazy reading in a useful way. When Tesla joined the S&P 500 in December 2020, it was the largest addition in the index's history, and observers including Research Affiliates flagged it as detached from fundamentals on standard valuation metrics. The lesson usually drawn is "index inclusion pumped Tesla." The more accurate lesson is that the price had already detached on narrative, and inclusion was a milestone in that story rather than its cause. The flow did not make the bubble. The belief did.

Narrative-supported prices behave differently from fundamentally-supported ones. They can run further than any model would justify, which is what makes betting against them so painful. And they can reverse without warning, because the thing holding them up, collective belief, is not continuous. It does not compress gracefully. It gaps.

A price held aloft by price-insensitive, narrative-driven demand, sitting on top of a conglomerate whose profitability is concentrated in one segment and whose control is concentrated in one person, is a textbook low-probability, high-impact configuration. The expected path can look calm and upward for a long time. The distribution of outcomes is not calm at all. The left tail is fat, and it is fat precisely because the support is psychological rather than mechanical.

This is the kind of setup that tail-risk thinking is built to price. The question is not "what is the stock worth on a discounted-cash-flow basis," because for a name like this, in a moment like this, that number is not what is setting the price. The question is "what happens to the price when the narrative that is setting it stops being told the same way." For a fundamentally-supported stock, bad news means a lower multiple. For a narrative-supported one, bad news can mean the floor was never there.

The Honest Counterargument

We owe you the other side, because it is strong, and because anyone who skips it is selling you a posture rather than an analysis.

Being early against a narrative-supported, founder-haloed mega-cap is one of the most dangerous positions in markets. The story can compound for years. Short interest becomes fuel: a stock that "should" fall can be forced violently higher when the people betting against it are squeezed, and SPCX will have every ingredient for a squeeze, including a passionate retail base and a founder who engages directly with it. The passive bid, weak as it is per share, is also sticky and one-directional once inclusion happens; index funds do not sell on valuation. And SpaceX genuinely might grow into the wrapper: Starlink is scaling fast, and a credible path exists where the profitable segment simply gets much bigger and the loss-makers turn. None of that is fantasy.

So this is not a call to bet against the stock, and we are not making one. It is a case for seeing clearly what the trade actually is.

Who Collects the Rent

Every offering has a question of who is on the other side. When the banks moved on stablecoins, we asked who collects the rent, and the answer was the incumbents reclaiming the rails. Here the question is sharper and more uncomfortable: at a price set by narrative rather than by the economics of the profitable core, public, retail, and retirement money is providing the exit liquidity for earlier insiders. That is what an IPO is, mechanically. The only question is whether the price at which that handoff happens is one the underlying business can grow into, or one that only the story can support.

The crown jewel is real. Starlink is a genuinely good business. But you are not being offered Starlink. You are being offered a wrapper around Starlink, with two loss-making segments inside it, control you do not hold, and a price set by how badly people want to own the name.

So how should you actually hold a name like this? First, value the segments, not the wrapper. The right mental model is a sum of the parts: a profitable connectivity business, a capital-intensive launch business, and a deeply loss-making AI business, each with its own trajectory and its own multiple. The blended ticker invites you to skip that work. Do not.

Second, watch the story, not the flows. The mechanical-flow worry is the wrong gauge. The gauges that matter are the ones that measure belief: retail positioning, narrative breadth, how much of the price depends on milestones rather than margins.

Third, do not confuse a great company with a great entry price. Those are different propositions, and the entire machinery of an IPO is designed to make you forget that they are.

The naive read is that a generational company finally went public and everyone wins. The structural read is that a profitable core arrived bundled, controlled, and narrative-priced, and that the most important variable is not the rocket or the satellite or the model. It is belief, and belief is the one input with no floor.

For informational purposes only. Not investment advice and not an offer or solicitation of any investment. See the full disclaimer.

Works Cited

Greenwood, Robin, and Marco Sammon. "The Disappearing Index Effect." Journal of Finance, 2025. Harvard Business School Working Paper 23-025.

Research Affiliates. Commentary on Tesla's S&P 500 inclusion and valuation metrics, 2020.

U.S. Securities and Exchange Commission. "Space Exploration Technologies Corp., Form S-1." 20 May 2026.

U.S. Securities and Exchange Commission. "Space Exploration Technologies Corp., Form 424B4 (Final Prospectus)." 12 June 2026.