The Empire Strikes Back: Are Banks Capturing the Stablecoin Revolution?

Eighteen months ago, the story was simple. Stablecoins were the insurgency.

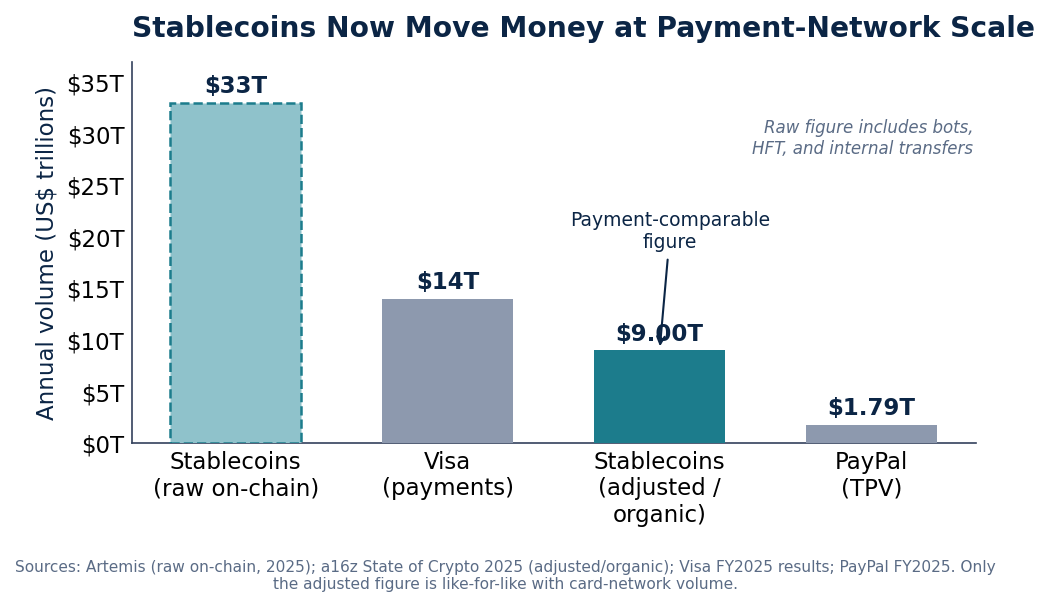

A dollar-pegged token had quietly rebuilt the plumbing of the dollar around the very banks that had controlled it for eighty years. The numbers were not subtle. Depending on how you count, stablecoins settled somewhere between $9 trillion and $33 trillion in 2025. The lower figure strips out bots, high-frequency loops, and internal transfers to isolate genuine economic activity; the higher figure captures every transfer on-chain. Even the conservative, bot-filtered number rivals Visa's roughly $14 trillion in annual payments volume. The raw number exceeds it outright. We called it the Liquidity Insurgency: the asset, the dollar, had finally been separated from the rails, the U.S. banking system that had always carried it. The hegemon, we argued, had surrendered control of the flow to the code.

This month, the hegemon answered.

In the span of a single week, four of America's largest banks (JPMorgan, Bank of America, Citigroup, and Wells Fargo) confirmed they are building a tokenized-deposit network through their co-owned Clearing House, a bank-controlled settlement layer targeting a first-half-2027 launch and a direct institutional counterpunch to dollar-pegged crypto. Days later came reports that Stripe, Visa, and Mastercard are standing up a competing stablecoin platform of their own, with Coinbase reportedly in talks to participate. Mastercard, not content to wait, has already widened stablecoin settlement across eight blockchains and extended card settlement into weekends and holidays. The incumbents are not watching from the sidelines anymore. They are building.

The mainstream read is that this is validation: Wall Street capitulating, finally embracing the technology it spent a decade dismissing as a toy for speculators and criminals. We think that read is exactly backwards.

Is This Disruption, or Capture?

There is a difference between adopting a technology and absorbing it.

When a challenger forces an incumbent to change, there are two ways the story can end. In the first, the incumbent loses: the new entrant keeps the advantages that made it dangerous, and the old guard is left managing a shrinking book of legacy business. In the second, the incumbent co-opts: it adopts the challenger's tools, strips out the parts that threatened it, and re-emerges with its position intact and its moat rebuilt in a more modern shape. The history of finance is mostly the second story. Money-market funds were going to disintermediate the banks; the banks now run them. Index funds were going to gut the asset managers; the largest asset managers now dominate indexing.

So when the incumbents who were supposed to be disintermediated start issuing the instrument themselves, the relevant question is not whether stablecoins won. They did. The question is who collects the rent now that they have.

Consider the timing, because the timing is the whole tell. The GENIUS Act's first hard deadline lands on July 18, 2026: the one-year mark when implementing regulations are due and the permitted-issuer application window opens, with the full regime taking effect in January 2027. A broader market-structure bill, meanwhile, carries an estimated 50–60% chance of passing before the midterms. Regulation that arrives at the moment of mass adoption rarely democratizes a market. It formalizes who is allowed to operate in it. Bank-grade reserve requirements, third-party audits, issuer licensing, capital buffers: each is defensible on its own terms, and each is also a cost. Costs are barriers. Barriers are moats. And moats are built, almost by definition, by the institutions that already have the capital to clear them.

The insurgency's whole premise was permissionless: a dollar living in a smart contract that no intermediary could freeze, reverse, gatekeep, or tax. The counterattack does not destroy that dollar. It does something subtler and more durable: it offers a sanctioned version, wrapped in the same familiar names, blessed by regulators and trusted by enterprise treasurers who would never touch an offshore token. Same rails, same speed, same programmability. Just with a gatekeeper restored at the door.

| Player | Initiative | Status |

|---|---|---|

| JPMorgan, Bank of America, Citigroup, Wells Fargo | Tokenized-deposit network via The Clearing House | Targeting H1 2027 launch |

| Stripe, Visa, Mastercard (Coinbase in talks) | Competing stablecoin platform | Reported, standing up now |

| Mastercard | Stablecoin settlement across eight blockchains; weekend and holiday card settlement | Live |

What the Incumbents Actually Get Back

To see why this is a counterattack and not a surrender, follow what the incumbents stand to reclaim. Re-intermediation is the prize, and it has three layers.

- The float. A stablecoin is, mechanically, a money-market fund with a payments interface: the issuer holds reserves (Treasuries, repo, cash) and earns the yield on them while the holder earns nothing. At today's rates, the interest on the float backing a large stablecoin is a multi-billion-dollar business, and for the past two years it has flowed to Circle, Tether, and a handful of fintechs rather than to the banks. A bank-issued stablecoin or tokenized deposit keeps that float, and the income on it, inside the banking system where it started. With the total stablecoin market already standing near $310 billion in outstanding supply, this is not a rounding error.

- The rails. Visa and Mastercard do not need to win the asset war to win the war. They have never been in the business of issuing money; they are in the business of moving it and charging a toll. Routing settlement across eight blockchains and clearing on weekends and holidays is not crypto-enthusiasm. It is the toll booth being relocated onto the new highway before the traffic fully arrives.

- The identity layer. This is the quiet one, and the most important. Whoever controls KYC, custody, and the compliant on-ramp controls who is allowed to transact at all. A sanctioned stablecoin is only usable through identified, permissioned access, which hands the issuer the power to approve, monitor, freeze, and reverse. That is the exact power the original stablecoin thesis was designed to route around.

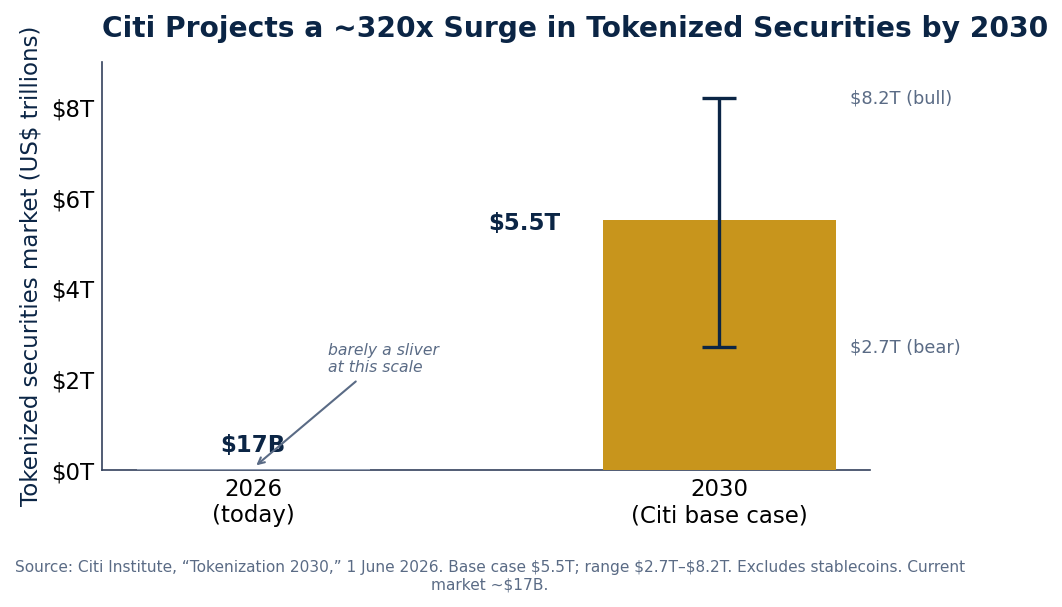

None of this is hypothetical upside. Citi projects the tokenized-securities market alone will grow from roughly $17 billion today to a base-case $5.5 trillion by 2030, with a bull case of $8.2 trillion, a move on the order of 300x in five years. The question that matters for your portfolio is not whether that number is directionally real; the infrastructure being built this month suggests it is. The question is which balance sheets capture it. And the answer, as the launches stack up, is consolidating, not dispersing.

The Investor's Mistake

The reflexive trade here is to treat bank involvement as a green light. The grown-ups have arrived; the asset class is legitimate; the risk is gone. Buy the thing the banks are now blessing. That is the conventional safe view, and as usual it is the actual risk.

A sanctioned, bank-issued, fully-KYC'd stablecoin is not the anti-hegemon. It is the hegemon in a new wrapper: faster and programmable, yes, but with all of fiat's surveillance and freeze-ability quietly restored. If your reason for holding a digital dollar was convenience, the bank version is strictly better: cleaner, safer, fully compliant. But if your reason was neutrality, exposure to a dollar that no single authority could switch off, seize, or sanction you out of, then the bank version gives you none of what you came for. It is a checking account with extra steps.

And here is the part that should reassure rather than alarm anyone holding the neutral version: the counterattack is the strongest confirmation yet of its value. You do not spend a decade dismissing a technology, then mobilize the four largest banks in the country and the two largest card networks on earth to build a controlled alternative to it, unless the uncontrolled original is worth taking seriously. Nobody builds a moat around something worthless.

| Sanctioned (bank-issued) | Neutral (censorship-resistant) | |

|---|---|---|

| Control | Issuer can freeze, reverse, censor | No single authority can switch it off |

| What you own | Yield and efficiency on the existing system | A hedge against a weaponizable dollar |

| Access | Permissioned, full KYC | Permissionless, multi-chain |

| Regulatory path | Smooth | Rougher, by design |

Positioning for the Counterattack

This is not a moment to abandon the trade. It is a moment to be precise about which version of it you own.

- Distinguish sanctioned exposure from neutral exposure. Bank-issued tokens and tokenized deposits are a yield-and-efficiency play on the existing system: a better pipe, not an exit from it. They will likely be excellent businesses and reasonable holdings. Just size them as fintech, not as a hedge against the system that issues them.

- Keep a position in genuinely neutral rails. The entire purpose of a hedge against a weaponizable dollar is that it cannot itself be weaponized. If an issuer can be compelled to freeze, censor, or reverse, it is not the hedge. It is the thing you were hedging against.

- Watch the moat, not the headlines. The launch announcements will keep coming, and most will be noise. The signal is structural: the July 18 GENIUS Act deadline and the market-structure bill will tell you more about who ultimately captures this market than any product reveal. Read the rules, not the press releases.

The insurgency proved the dollar could be separated from the bank. The empire's reply is to put the bank back on top of the dollar: quietly, compliantly, and with the regulator's blessing. The technology won. The open question, as always, is who gets to own the win.

Works Cited

a16z crypto. "State of Crypto 2025." Andreessen Horowitz, 22 Oct. 2025.

Artemis Analytics. "Stablecoin Payments From the Ground Up, 2025." Artemis, Jan. 2026.

Citi Institute. "Tokenization 2030: Wall Street On-Chain." Citi Global Perspectives & Solutions, 1 June 2026.

CoinDesk. "JPMorgan, Bank of America and Citi Are Going on the Blockchain Offensive With a Shared Tokenized Network." 5 June 2026.

CoinDesk. "Payment Giants Stripe, Visa, Mastercard Said to Be Among Backers of Soon-to-Debut Stablecoin Platform." 3 June 2026.

Mastercard. "Mastercard Expands Settlement Capabilities to Include Stablecoins." Mastercard Newsroom, June 2026.

PayPal Holdings. "Fourth Quarter and Full Year 2025 Results." 2026.

Visa Inc. "Fiscal Full-Year 2025 Operating Results." Oct. 2025.